Hey! I’m @yourboymilt, and welcome to retail’s Sunday Paper.

I should probably let you know...This is not financial advice! We are here to entertain while giving you ideas, perspective, and angles. Do your own research, I prithee. And if you aren’t subscribed, join us here:

Pt. 1: Week’s Thoughts, Pt. 2: STOCK Act DD (Raimund J. Stieger]), Pt. 3: The Medallion Fund DD (@mkt_sentiment), Pt. 4: Guest Watchlist (@wealthbrah), Pt. 5: Index Forecasts (@daarkmaagician ) Pt. 6: Beyond the Screen, Pt. 7: TLDR

At some point, in the unending boredom accompanying the most interesting spring of our generation, from widespread poverty sprang endless opportunity. Of course, our fast plunge into a slow market came from the freedom of time provided by home confinement—lest we spend our newly gifted hours outside, audaciously participating in our previously known monotony.

“That Chad” they’d say through gritted teeth “is quite an awful young man these days. He’s running errands all around the city, going with friends to hike, and he’s even working out at the gym! I’m certain I saw him at a restaurant with his fiancée just last week...that poor woman has settled down with quite the monster.”

What a time to be alive it was, is, and according to my bleeding BA calls may always be.

At that point most of us were too short on cash to go long on an Amazon, and the investing choices became more and more risky for the sake of financial safety. The old, small companies—the ones who couldn’t afford to keep their own doors open—opened the doors to large gains and afforded small accounts big opportunities. New races for the bottom sent accounts to the top, and investors eyed the next failure to bring about their success.

Investors are piling into stocks of companies in bankruptcy, wagering against a court process that routinely wipes out shareholders.

Car renter Hertz Global Holdings Inc., oil driller Whiting Petroleum Corp. and retailer J.C. Penney Co. are among companies that have seen their shares more than double in recent trading sessions despite being in Chapter 11 bankruptcy, a process that allows companies to keep operating while working out a plan to repay creditors.

Then they came. For those taking the safer route of risky investing, the large gains from small companies became obsolete—that’s when the option of options was discovered. My first illuminating conversation with a friend, from what I can recall, went something like this…

‘If you can’t afford the company then you buy an option for the stock, then you’ll share in the success of the stock without owning any shares of the company.’ He said.

‘So I’d own the shares, then?’ I replied with confusion.

‘No. You have the option to make a profit buying the shares at expiration, which won’t happen because you’ll sell the options before they expire.’

‘So, once my options for the stock are expired, I’ll then be an owner of the shares?’

‘What? Don’t be silly. You just said you can’t afford the shares—so, then, you can only afford the options for the company’s stock.’

‘The options which give me the right to buy shares of the company?’

‘Yes.’

‘But I don’t want the actual shares of the company?’

‘Absolutely not.’

‘So my only option, then, is options?’

‘Exactly.’

And what a ride it’s been since then. Robin Hood—the opportunity for small investors to gain profits off of large corporations—was outed as an opportunist protecting those corporations from the loss of large profits off of small investors. They’re an ordinarily evil company doing extraordinarily well, treating good customers bad like any good company should.

The modern FURU has fed us promises of freedom while providing us with shackles; they tell you to buy stocks at the bottom which they then sell into a top you’ve caused, until the stocks you once held at the top reach a new bottom that won’t be topped. Guess they’ve got us so busy watching their watches that we don’t watch the stocks that they drop from their watchlist. F.

Sadly, when we band together the FURUs aren’t the only gurus against us; the once-profitable betters on Wall Street place blame on the prophets of Wall Street Bets. We’re apparently short-sighted gamblers who illegally make markets move, when we’re really keeping market makers from moving their shorts illegally.And now, their biggest enemy is the S.E.C. Chair:

During a Wednesday interview, CNBC’s Jim Cramer asked U.S. Securities and Exchange Commission chair, Gary Gensler, whether the SEC should step in to prevent a coordinated effort by Reddit investors to “smash” short sellers who bet against popular meme stocks like GameStop Corp. GME, -0.68% and AMC Entertainment Holdings Inc. AMC, -4.00%

“If three hedge fund members work in concert to smash a short hedge fund, the 5 million Reddit people would say that’s legal, but perhaps it shouldn’t be,” Cramer said. “If 5 million people decide to smash a hedge fund that’s short, is that ok? What’s within the bounds of what you can do to smash a short seller?”

Meme dreams aren’t the only things in the balance as of late; the 50 day moving average on the previously well-performing SPX indicates it’s actually performing less than average. Bulls are beginning to feel as unwell as any bearish bull should, but in this case market fears should turn to market flight;

The 50-Day MA discussion has been pounded into our heads with every drawdown,” writes Frank Cappelleri, desk strategist at Instinet. “And while we may be sick of hearing about it, the dip buying around the line has been a real phenomenon.

Now, as in that 2020 of profitable pandemonium, we’ll bet on the rich products of poverty. The FOMC meeting this week is the meeting of all meetings, and we need the economy left for the dead for the market to stay alive. The Fed will meet this week to determine if we’re still too weak to put a start to the end of liquidity that’s expected to dry up.

When it meets on Sept. 21 and 22, the Federal Open Market Committee (FOMC) will likely continue to weigh whether it should buy fewer bonds—or if it should continue to hold off on tapering those purchases until the economy is on firmer footing.

For months now, market observers have been waiting with bated breath for the day Federal Reserve Chair Jerome Powell will announce such a move.

As Powell made clear in his Jackson Hole speech last month, the economy has not sufficiently convalesced. There are still millions fewer workers employed than before the onset of the pandemic, and the weak August jobs report shows that a fast recovery isn’t in the cards.

So, if the economy is sick enough then the market will react well enough that it’ll put our call options back in play. Should we be worried? Meh, I’d think not if we’ve come this far; we’re immature investors, yet we’ve made more investing than the others who give their investments more time to mature. Hopefully things don’t go so poorly you start to YOLO outside the money options, trying to dig yourself out from inside the hole you’ve FOMOd yourself into.

The market is not the economy and the economy is not the market; one consists of lives navigating the broken promises of our nation, while ours is a practical manifestation of speculative fervor. Unfortunately there is only one catch and it’s Catch 22; the more money they make, the more money we lose.

Welcome to YEET no. 22, brought to you by the need for a second read through.

🏦 Pt. 2: Can the STOCK Act Actually Prevent Members of Congress from Trading Stocks?

Written by: Raimund J. Stieger

* = footnotes (listed in the order they appear)

In 2012, Congress passed the Stop Trading on Congressional Knowledge Act of 2012 (the “STOCK Act”) to combat insider trading occurring within the Executive branch. The STOCK Act prohibits members of Congress, Congressional employees, and executive branch employees designated as public filers “from using nonpublic information derived from or obtained through their official positions for personal benefit and other purposes.”* Congress passed the STOCK Act because, prior to its enactment, members of congress could legally make trades utilizing the nonpublic information they learned through their congressional duties.* The fact that it took until 2012 for such an act to be passed may come as a surprise, especially to the framers who wrote of “old corruption” and “rotten boroughs”* two and a quarter centuries earlier.

Despite the STOCK Act not being passed until 2012, the United States has not been sitting idly by in its fight against corruption. Over the years Congress has passed the Federal Election Campaign Act focusing on increasing the public disclosure for federal campaign contributions, the Foreign and Corrupt Practices Act formally prohibiting the bribery of foreign public officials, the Ethics in Government Act establishing the Office of Government Ethics as an independent federal agency, the Inspector General Act allowing inspector generals to operate independently within their respective agencies, and other anti-corruption focused legislation. Many of these Acts Congress implemented in response to public opinion or current affairs of the time, such as the Ethics in Government Act that Congress passed in response to the Watergate scandal. Each of these Acts created a means of prosecuting offenders, as the Constitution does not give Congress the authority to enact general criminal offenses. All federal offenses are based on one or more of Congress’ enumerated legislative powers.

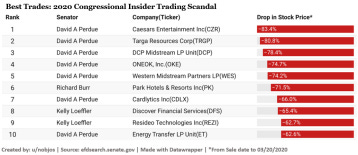

Despite Congress’ passage of a plethora of federal legislation designed to weed out and prevent corruption, the Department of Justice (the “DOJ”) has never successfully prosecuted a member of Congress or an employee of Congress for violating the STOCK Act.* Recently, several members of Congress were investigated for insider trading scandal after they sold millions of dollars of stocks after being briefed on the COVID pandemic* and days before the Dow Jones’ fell nearly 3,000 points on March 16, 2020*—the largest single-day drop in U.S. stock market history. Figure 1 shows the top ten trades made during this scandal.

Figure 1: Ranked from most to least profitable, the above table shows trades made by Senators and the resulting drop in the company’s stock after the March 16th crash.*

Despite the public outcry and clear financial gain these senators obtained, both the FBI and the DOJ found the Senators to have not violated the STOCK Act. Senator Perdue, one of the Senators investigated by the DOJ, was able to avoid $2.2 million in losses by liquidating a significant portion of his portfolio—dumping $1.7 million worth of stock in thirty-three transactions—weeks before the March 16th crash.* The overwhelming appearance that these Senators gained financially from nonpublic information is, however, not sufficient to justify prosecuting a sitting Senator. As such, the DOJ announced in January of 2021 that it was dropping its investigation into Senator Burr’s alleged STOCK Act violations.

While the DOJ does not comment publicly on its rationale behind its decision to prosecute, it is likely that the DOJ did not believe it could overcome the two large obstacles protecting members of Congress: The Speech or Debate Clause and proving the “materiality” of the nonpublic information given the unique circumstances surrounding the trades. The Speech or Debate Clause states that “[t]he Senators and Representatives shall...in all Cases...for any Speech or Debate in either House...not be questioned in any other Place.”* This premise provides members of Congress with general criminal and civil immunity for acts taken in the course of their official duties to protect them from intimidation by the other branches of Government.* The D.C. District Court upheld this premise in United States v. Rayburn House Office Building,* where it held that the FBI had violated Representative William Jefferson’s constitutional right under the Speech or Debate Clause and ordered the return of documents covered under the Clause’s privilege.*

The framers, in their writing of the Constitution, intended to protect members of Congress from possible corruption or a hostile judiciary. Their well-intentioned drafting has shown that some people can wield shields as swords. A determined individual could, as it was seen in Rayburn, use the protections provided by the Speech or Debate Clause to cripple any would-be prosecutors from obtaining the evidence necessary to get a conviction. It cannot be said with certainty that the significant hurdle presented by the Speech or Debate Clause impacted the DOJ’s decision to drop its investigation, but it can also not be ruled out.

Even if, in arguendo, prosecutors were able to overcome the protections laid out by the Speech or Debate Clause and obtain documents showing that a member of Congress had nonpublic information, there exists a second hurdle—proving materiality. Under the Federal Rules of Evidence, evidence is material only if it is logically connected to a fact of consequence that is in question and that fact in question can impact the outcome of the case.* For example, the Periodic Transaction Report Speaker Pelosi filed on July 2, 2021 listed that her husband purchased between $1–5 million worth of call options for Alphabet in mid-June.* Speaker Pelosi’s vote on the House Judiciary Committee later that month on the House’s ongoing tech-focused antitrust efforts resulted in her husband’s options netting $5 million in profits.*

A brief reading of the facts may cause a reader to infer that Speaker Pelosi violated the STOCK Act by making this trade, but the DOJ neither investigated nor prosecuted her. That may be in part due to an inability to prove that Speaker Pelosi had access to nonpublic information that was material in her husband purchasing those call options. Speaker Pelosi has also stated that “[she] has no involvement or prior knowledge of [her husband’s Alphabet call options purchases].”*

Prosecuting insider trading can be difficult, even more so when it involves members of Congress, but that difficulty should not be the reason for a lack of enforcement actions. The difficulty should be motivation for prosecutors and investigators to work that much harder at rooting out corruption in the legislature.

The National Bureau of Economic Research published an empirical study in April of 2020 that found, after the passage of the STOCK Act, members of Congress generally underperform the market in the short term and slightly outperform the market at the one-year mark.* These findings imply that when a member of Congress makes an extraordinarily successful short term trade it is against the statistical norm. Purchasing over one million dollars of call options, as Speaker Pelosi’s husband did in June, that results in over $5 million in profit is an outlier and outliers should be investigated.

Yet, after eight years since its passage, not a single member of Congress has been prosecuted for violating the STOCK Act. While Representative Collins was imprisoned in 2020 for insider trading, it was for his role as a board member with a biotech company and unrelated to his legislative duties. An option that, while radical in 2012, may be feasible in the current political climate could be to provide strict trading and investment limitations for members of Congress, like restrictions employees of the Securities and Exchange Commission (“SEC”) are subject to.* Given the vast amount of information members of Congress have access to, it is likely that the Office of Congressional Ethics could not feasibly review all requests in a reasonable amount of time.

Therefore, a more economic solution would be to restrict members of Congress to trading only sector funds or diversified mutual funds. Such a restriction would remove the two major hurdles currently impacting the DOJ’s ability to prosecute STOCK Act violations. Essentially eliminating the possibility of members of congress making possibly unethical trades. In addition, members of Congress should pride themselves in being held to a higher standard than the average American. By allowing their colleagues to take advantage of the framers’ good intentions. The constitution should be a shield protecting the people, not a sword for financial opportunists capitalizing on America’s trust.

Footnotes:

1 Stop Trading on Congressional Knowledge Act of 2012, Public Law 112–105. 2 Zeke Miller, '60 Minutes' Blows the Lid Off Congressional Insider Trading, Business Insider, (Nov. 14, 2011), https://www.businessinsider.com/congressional-insider-trading-revealed-on-60-minutes-2011-11. 3 Rotten boroughs being a historical British term used to describe an election district with a small or declining electorate that retained its original representation in parliament. These boroughs were frequently represented by a member of the district’s patron family that, generally, did not vote in the interests of their electorate. Resulting in unfair representation in parliament. 4 Karen Woody, Criminal Laws to Combat Corruption and Prosecutorial Discretion in Enforcement of Anti Corruption Laws (June 15, 2021). 5 See Sen. Kelly Loeffler Dumped Millions in Stock After Coronavirus Briefing, The Daily Beast, (March 20, 2020) https://www.thedailybeast.com/sen-kelly-loeffler-dumped-millions-in-stock-after-coronavirus-briefing; David Perdue's stock trading saw an uptick as coronavirus took hold, The Atlanta Journal-Constitution, (April 7, 2020), https://www.ajc.com/news/state—regional-govt—politics/david-perdue-stock-trading-saw-uptick-coronavirus took-hold/MRWmzwXeHgxi6IcmBbPgaN/; Senate Intel Chair Unloaded Stocks In Mid-February Before Coronavirus Rocked Markets, OpenSecrets.org, (March 19, 2020), https://www.opensecrets.org/news/2020/03/burr-unloaded stocks-before-coronavirus/. 6 Kimberly Amadeo, How Does the 2020 Stock Market Crash Compare With Others?, The Balance, (updated, June 1, 2021), https://www.thebalance.com/fundamentals-of-the-2020-market-crash-4799950. 7 This information was collected through efdssearch.senate.gov which allows the public to search the periodic transaction reports (Office of Government Ethics Form 278-T) of members of Congress. The OGE 278-T is a mandatory form that requires public filers to disclose any financial transaction above the $1,000 de minimis threshold within thirty days. 8 Id. 9 U.S. Con. Art. I, §6, cl. 1. 10 Todd Garvey, Understanding the Speech or Debate Clause, Congressional Research Service, (Dec. 1, 2017), https://fas.org/sgp/crs/misc/R45043.pdf. 11 See generally 497 F.3d 654 (D.C. Cir. 2007). 12 Id. at 667. 13 See Fed. R. of Evid. 401. 14 Nancy Pelosi, Periodic Transaction Report (July 2, 2021), https://disclosures-clerk.house.gov/public_disc/ptr pdfs/2021/20019004.pdf. 15 Antoine Gara, Inside Nancy Pelosi’s Husband’s $5 Million Alphabet Options Windfall, Forbes, (July 8, 2021), https://www.forbes.com/sites/antoinegara/2021/07/08/inside-nancy-pelosis-husbands-5-million-alphabet options-windfall/?sh=b06bd8db8575. 16 Id. Quoting Speaker Pelosi’s spokesperson Drew Hamill (internal quotations omitted). 17 William Belmont et. all., Relief Rally: Senators As Feckless As the Rest of Us at Stock Picking, National Bureau of Economic Research, (April 2020). https://www.nber.org/papers/w26975. 18 Employees of the SEC, under OGE regulations and SEC supplemental regulations, cannot trade a security without receiving prior clearance from the SEC Ethics Office.

🦔 Pt. 3: The Medallion Fund - The greatest hedge fund of all time!

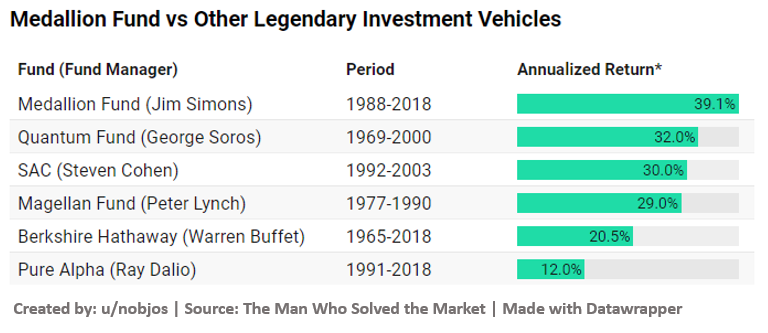

Jim Simons, the founder of the Medallion Fund has done what most people consider to be impossible. His fund has consistently beaten the market over the last 30 years. The fund has had an average return of 66% before fees during the period of 1988-2018!

To put these returns in perspective, $100 invested into the Medallion Fund in 1988 would have converted into $398 Million by 2018. Even net of fees [1], the fund has outperformed S&P 500 returns by ~1000 times and Warren Buffet’s returns by ~200 times!

If you are still not convinced about the absurdity of the returns, take a look at the following chart which showcases the annual returns for the Medallion fund in comparison with S&P 500.

Notice anything strange? Since its creation, the fund has only lost money in a single year [2] (1989). For the next 30 continuous years, there was not even a single year where their returns dropped below 20%. Even at the peak of the 2008 financial crisis, the fund had made an 82% gain net of fees!

We all know that Hedge Funds gets a lot of hate, most of the time justifiably so. But returns like this sustained for such a long time period call for further scrutiny. So in this week’s analysis, we are deep-diving into how the Medallion Fund created such outsized returns for its investors.

The Beginnings

Jim Simons has a Ph.D. in Mathematics, taught math at MIT, and has worked for NSA as their codebreaker before turning his attention to the stock market. He was one of the first people who realized that pattern recognition could be applied to beat the stock market.

He created a trading system that uses quantitative models and formed Renaissance Technologies in 1982. The peculiar thing about this hedge fund is that it does not hire anyone from financial or business backgrounds.

If Jim Simons wrote Avengers script

They solely focus on physicists, statisticians, mathematicians, and signal processing experts and believe that the herd-like mentality of business school graduates leads to poor returns! Renaissance’s headquarters is famously known as the world’s best physics and mathematics department.

This view is extended to their investment philosophy as highlighted by Robert Mercer (Co-CEO), Medallion Fund only focuses on the quantitative model recommendations and not the underlying business performance/strategy [3].

Fund Performance

I know we discussed the extraordinary returns of the fund in the beginning, but the following chart will put the sheer numbers into perspective.

By now we know that the fund has outperformed the S&P 500 index by a wide margin. But in this research paper by Bradford Cornell (Finance Prof at UCLA), he argued that even if the investor had the ability to predict the stock market returns perfectly on a monthly basis (shift the money to treasury during downturns and back to stocks during the upswings), the investor would only have been able to turn the $100 into $331K (an insane 331,100% return) but even this would be nothing in comparison to the ~$400 MM return generated by The Medallion Fund.

It’s not often you see Warren Buffet so low down a list for long-term investment returns. The Medallion Fund has beaten all the well-known investment managers by a wide margin over its 30 year period.

Fund Strategy

While the exact inner workings of the fund are only known to a few key insiders who are tightly bound by confidentiality clauses, what we know comes mainly from the book ‘The Man Who Solved The Market’ by Gregory Zuckerman [4].

As per the book, Medallion strategy involves holding thousands of short-term long, and short positions (aka like your avg r/wallstreetbets user) at any given time. Allegedly, they win 50.75% of the trades they make (not like your avg r/wallstreetbets user) which is enough to make them billions as they are conducting millions of trades every year.

Adding to the excellent quantitative models they have created, Medallion Fund also did two things right

1. Leverage:

It’s estimated that Medallion trades with 12.5x leverage on average with it going up to 20x when the system is confident. If you remove the leverage from the picture, the fund’s returns are similar to S&P 500. It’s their effective usage of leverage and deep understanding of risks involved that makes their returns legendary

2. Fund size cap: The fund has made sure that their Asset Under Management (AUM) never goes beyond $10Billion. They understand that adding more money might not work with the same strategies and have paid out their returns to their investors to keep the AUM same.

What does this mean for an average investor?

The Medallion Fund has been closed to outside investors since 1993. As of now, only the existing and previous employees of the company can invest in the fund. The funds of Renaissance that are open to the public have performed so poorly that the two funds made it the HSBC’s top 20 losers list for 2020.

While it certainly is a bummer that the average investor cannot invest in the fund, this analysis gave us some key insights into the market. The first and most important being that the stock market is not perfectly efficient and that there are inefficiencies that someone can leverage for more than 3 decades. The second being that not all funds that charge an exorbitant fee structure [1] are taking money away from the investor. In Medallion’s case, they are justifying their eye-watering fee structure with phenomenal returns.

Finally, this should not be considered as a call to action to find similar funds as not every team with stellar people end up producing market-beating returns [5]

Conclusion

It’s like Jim Simon’s had created a license to print money with the Medallion Fund. How long the fund’s algorithms can remain a secret and continue generating market-beating returns is anyone’s guess. My incredulity and skepticism during this analysis was perfectly captured by Bradford Cornell in his research paper

During the entire 31-year period, Medallion never had a negative return despite the dot.com crash and the financial crisis. Despite this remarkable performance, the fund’s market beta and factor loadings were all negative, so that Medallion’s performance cannot be interpreted as a premium for risk bearing.

To date, there is no adequate rational market explanation for this performance.

Until next time…

Footnotes

[1] The fund charges an exorbitant amount of fees. From 2002 onwards, it has a 5% management fee and 44% performance fee. To signify the impact of this fee, let’s take the following e.g. if you invest $100K into the fund and at the end of the year, your fund grows to $130K (a 30% return), they would charge you $5K (5% management fee) + $13.2K (44% of the profit) for a total of $18.2K in fees. So your net returns would only be 11.8%. Even if they lose money, they will still charge you $5K for managing your money. Vanguard SP500 ETF would charge you $30 for the same!

[2] Even in the year, their returns were negative, the fund returns before the fee were + 1%. The 5% management fee pushed them to the -4% net returns.

[3] His exact quote was “sometimes it [the model] tells us to buy Chrysler, sometimes it tells us to sell”

[5] Long Term Capital Management - A fund that was managed by a bunch of PhDs and Nobel laureates. It had posted great returns since starting in 1995 (in the 40% range) only to be bailed out in 1998, and was dissolved in 2000)

Hey YEETers, we've got a special guest in the house! I've been watching @wealthbrah (follow him) do his thing, quietly killing it with a combination of flow and charting. We got to talking on Twitter and I thought myself, "Well, shit, why not have my mans do a guest watchlist"...and here we are. He's dropped his plays and his thoughts with charts, and he has a unique approach to whale spotting that is definitely a different style than mine.

Without further ado I present to you....The WealthBrah Watchlist....

👀 Watchlist: SPOT, FSLY, DKNG, SPCE

1. SPOT

📊 SPOT: Chart

If price clears 250 (yellow region), it can move towards 257-260 (blue region).

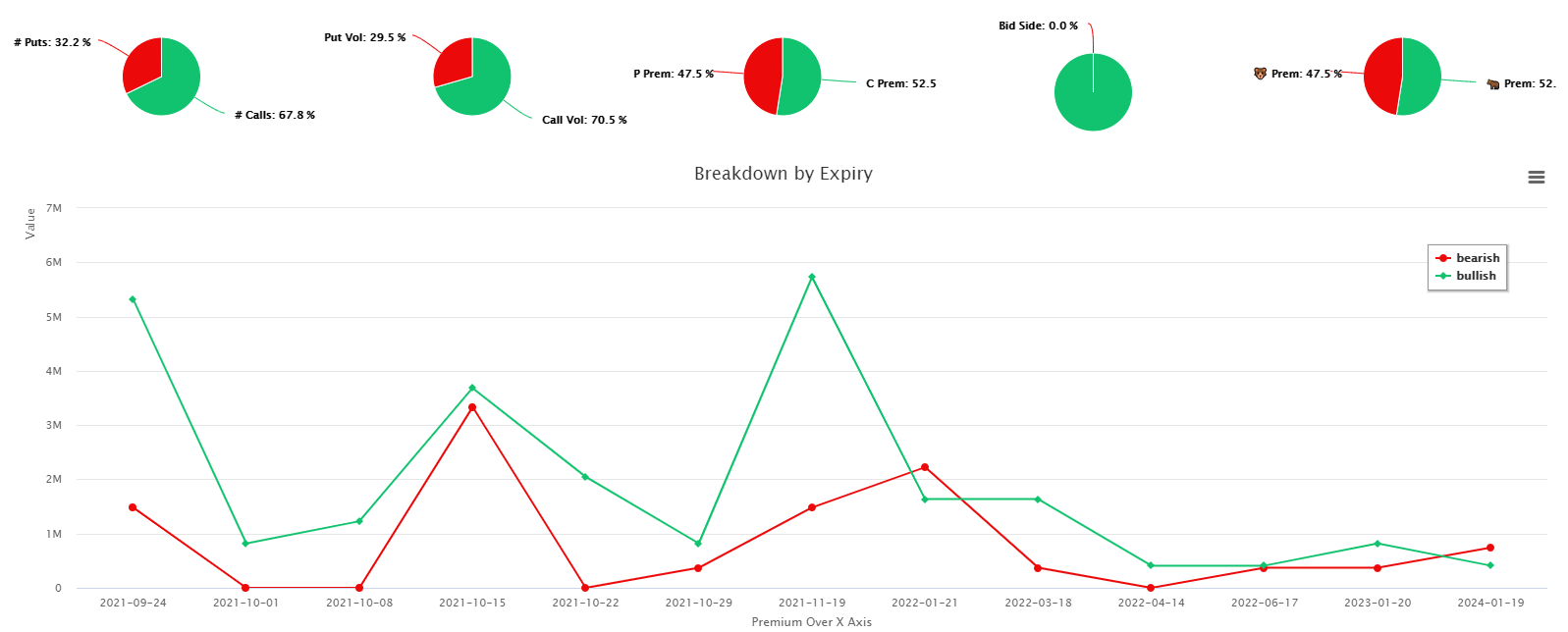

📈 SPOT: Flow Chart

$2.5k+, ask-side flow on 9/17 shows bulls aggressively targeting 9/24 and 11/19 strikes.

🌊 SPOT: Flow reading

Big whale unloading puts on the bid-side. The biggest trade on 9/17 was a $400K sell for 2024 puts. The second biggest trade (not pictured below) was a $320K sell for 2022 puts.

2. FSLY

📊 FSLY: Chart

Price over 45.50 can move towards 48. Price below 43 can move towards 40.

📈 FSLY: Flow Chart

$2.5k+, ask-side flow slightly favors the bears - high premium spent on 10/15 calls & 12/17 puts.

🌊 FSLY: Flow reading (5k+ Premium)

3. DKNG

📊 DKNG: Chart

Price above 61 can move to 64. Price below 58.50 can move towards 56 (in case the market turns bearish).

📈 DKNG: Flow Chart

$5k+, ask-side flow is 65% bullish, with bulls targeting short and long term calls.

🌊 DKNG: Flow reading (5k+ Premium)

4. SPCE

📊 SPCE: Chart

Price above 26.75 can move towards 28.50. Price below 23.50 can move towards 21.

📈 SPCE: Flow Chart

5K+, ask-side flow is almost dead even.

🌊 SPCE: Flow reading

Some of the biggest trades on 9/17 include puts worth $1M+ sold on the bid side & $100K spent on OTM monthly calls.

Thanks @wealthbrah! Excited to see how these play out.

Alright, here’s some from the gang:

The YEET Picks:

📞 Calls:ZM, SQ

🎲 Earnings BONUS: SFIX Calls

1. 👴Uncle ABU’s Fav: ZM Calls >292.56

He’s been beating the drum on this one all weekend, and has made a believer of many of us. It had a good run Friday on a super red trading day, and the chart says it’s just getting started.

He took a break from Stanning for FB to finally deliver another pick—SQ! An old favorite of mine, this one’s been priming the pump and looks ready to make a big move.

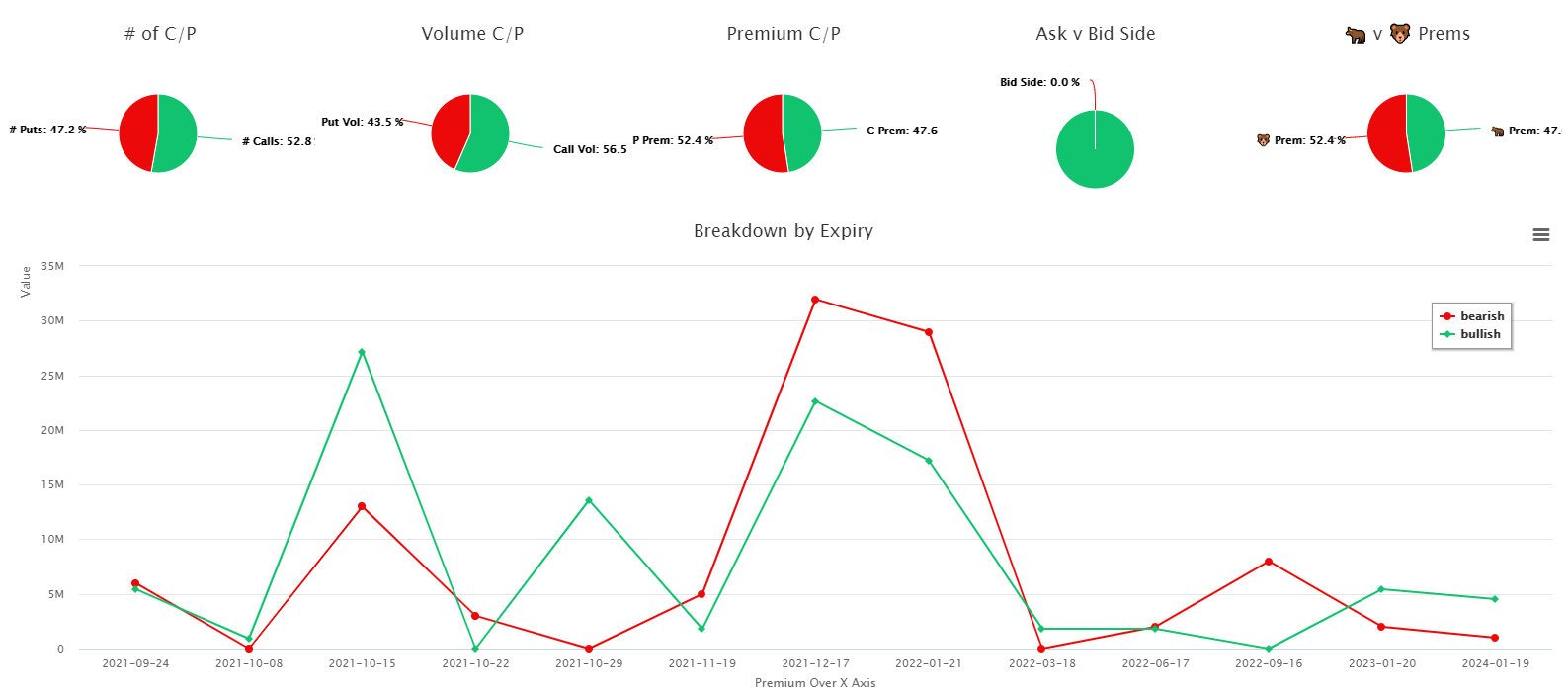

📈 SQ: Flow Chart

Flow 15k+: 77%🐂

⌚️SQ: Expirations and Strike

⌚️Exp: 9/24, 10/7, 10/15🐂 🔨Strikes: 245, 260🐂

📊 SQ: Chart

🔫 The Trigger: 257.3

🎲 Milt’s ER Bonus Gamble: SFIX Calls

Be warned: straight lotto, it’s either 100% gains or you lose it all—no in between guys.

IF I played earnings, I’d say that they’ve been beaten to a pulp and expectations are low. Often a good launchpad for a moon mission on a surprise of any type.

IF I played earnings, I’d say that they actually turned around their previously weak profitably numbers and that their CEO tends to deliver surprises, for better or for worse.

IF I played earnings, I’d say this chart is fuego and IF they did pull off a beat they have a ways to go up.

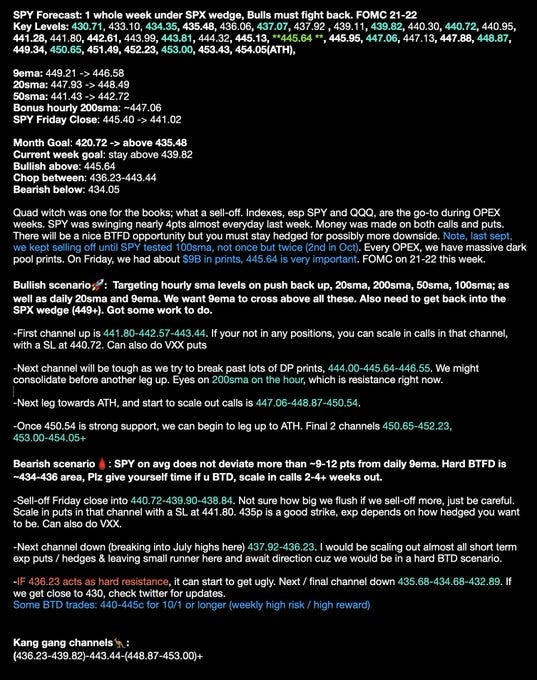

Pt 5: Weather: SPY/SPX & QQQ/TQQ Forecast by @daarkmaagician 🌦

Below is the chart & info for a SPY & QQQ forecast (plus some SPX & TQQ) from @daarkmaagician, his DISCORD is the place to be (YEETers get two weeks free!).

Charts Legend:

Solid Blue= ATH, Green= Dark Pool Buys, Red= Dark Pool Sells, Purple= Dark Pools, Orange= Supports/Resistances, Teal= 9ema

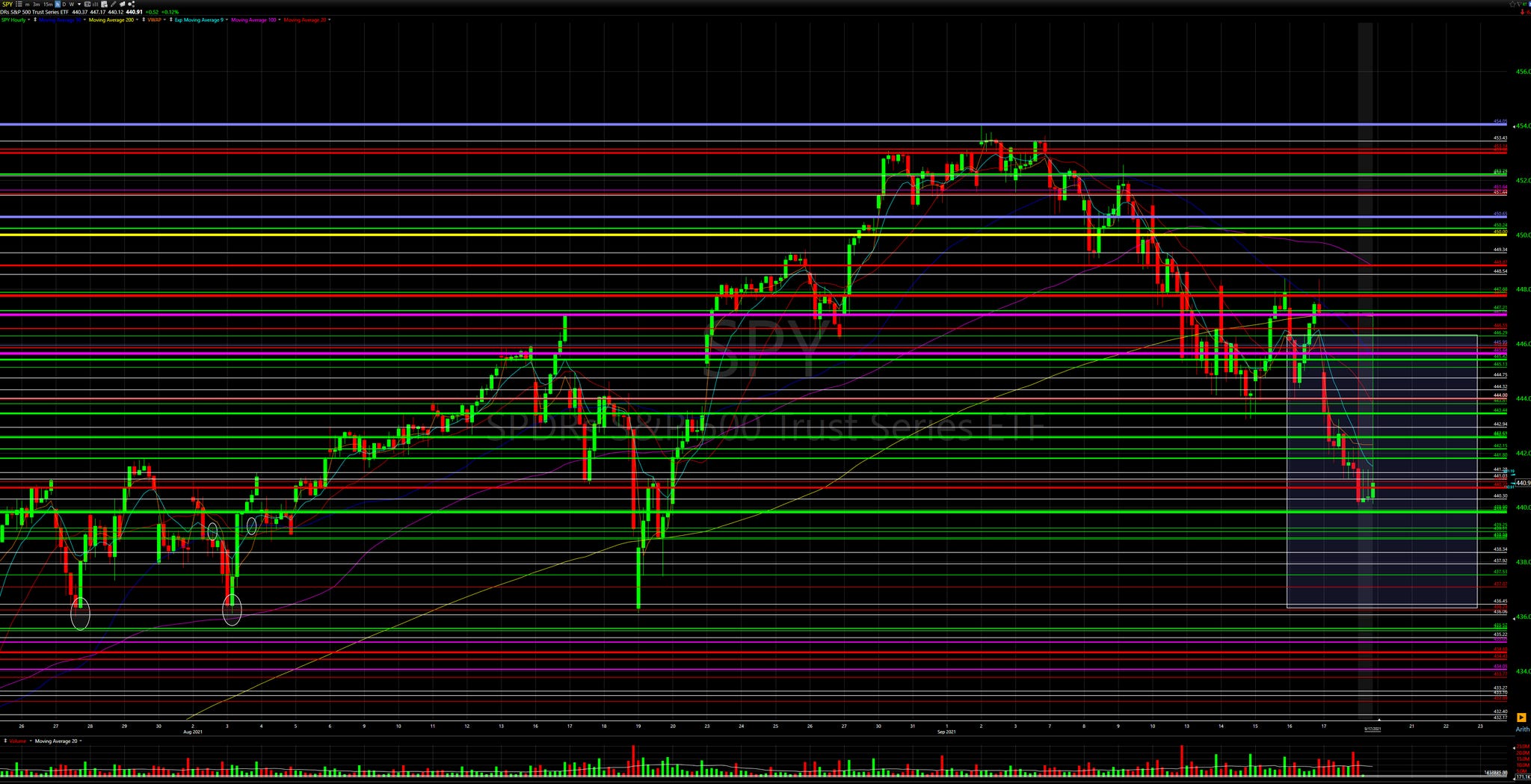

SPY Forecast:

SPX/SPY Forecast Charts:

SPX Weekly Chart: 2 back to back red weeks, 1 week closed under wedge

SPX Hourly Chart

SPY Hourly Chart

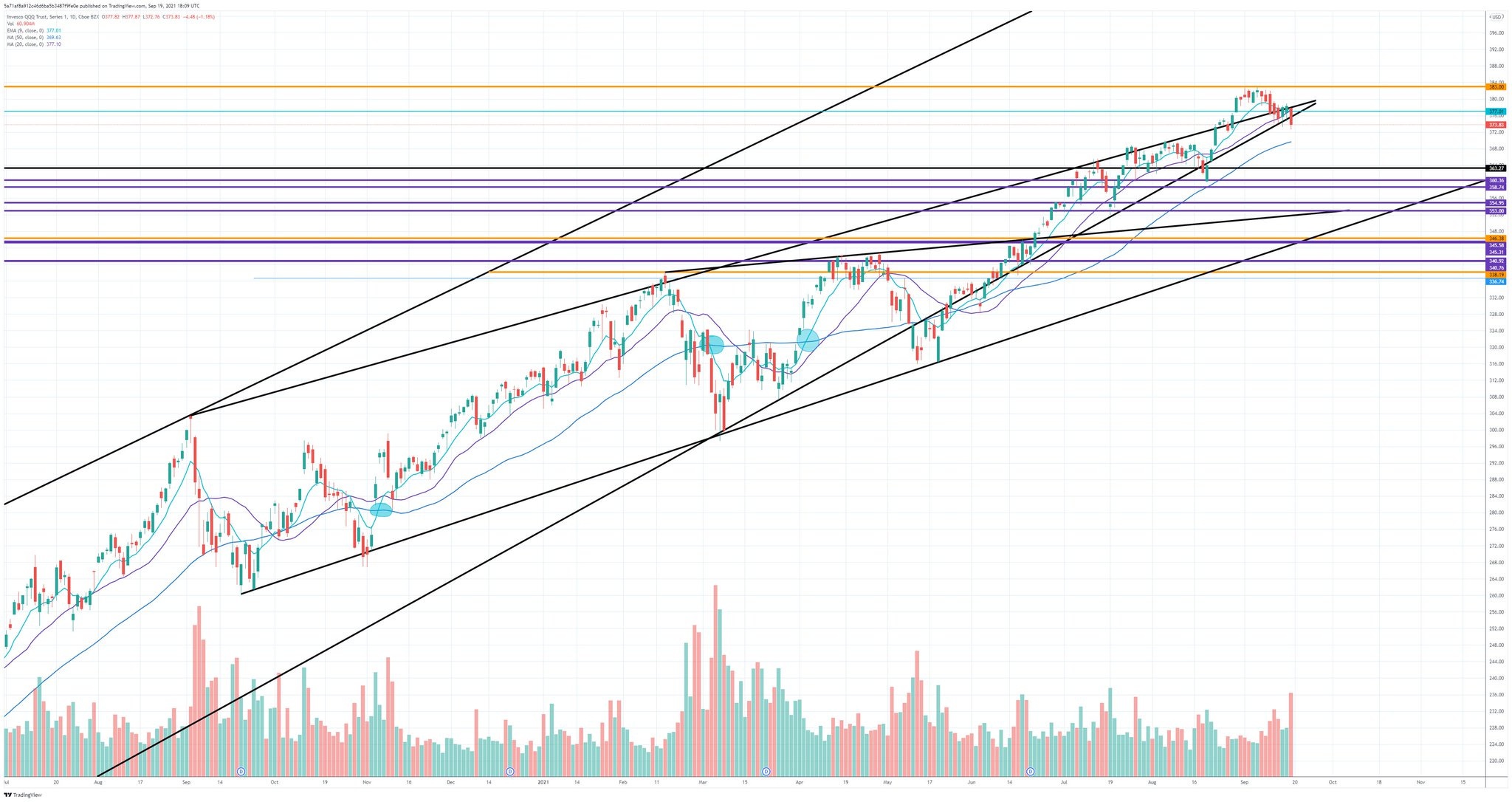

QQQ Forecast:

QQQ/TQQ Charts:

QQQ DAILY CHART

QQQ HOURLY CHART

Here’s TQQQ 200sma support / resistance / make or break

Make sure you follow @daarkmaagician to get updates on the indexes daily!

🌭 Pt. 6: YEET Team Beyond the Screens: Costco Eats

Each week The YEET Team will now feature something (God knows what) that has nothing to do with stocks, because apparently there’s more to life than stocks. This week, because our whole squad is obsessed with Costco, we’re giving you three strong BUY recommendations while you do your Sunday shopping. Now presenting: The YEET’s Eats—Costco Edition.

Fine dining for the YOLOer on the go

TPG’s favorite: The Costco Almond Danish

When it comes to deliciousness TPG has got it on lock, and he spent all week hollering for these things to get a shoutout in YEET. I’m watching post-COVID calories so I can’t indulge, but shoot me a message and tell me how it is.

@Modal_enigma’s Favorite: The Kirkland Prosecco

Kirkland and Prosecco are two words that shouldn’t go together, but Modal swears by this shit. He’s easily the most classy YEET Contributor—he even wears a tux in his Twitter profile—and legend has it his Chicago penthouse smells of sandalwood and fine leather.

Milt’s Fav: The Costco Hot Dog

Coming in at a respectable 580 calories, this is definitely the health food snack of the Costco world. I had one yesterday, I’ll have one next weekend, and so on and so forth until the end of time. Ketchup and mustard only; relish and onions on a hot dog is for weirdos just like pineapple on a damn pizza. Yeah, I’ve said it.

Tune in next week! Who knows what we’ll be up to!

Pt. 7: TLDR & GOODBYE ✌️

TLDR:

Pt. 2: The Medallion Fund: The Greatest Hedge Fund of All Time—deep-dive into how the Medallion Fund created such outsized returns for its investors.

Pt. 3: Can the STOCK Act Actually Prevent Members of Congress from Trading Stocks?